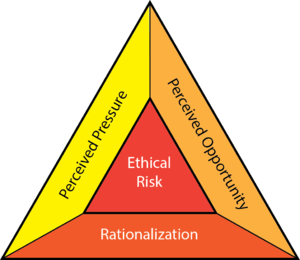

We have known about the fraud triangle for decades. Fun fact: it has three sides.

Yet, whenever we identify fraud in the organization, our automatic reaction is to work on reducing opportunity. Opportunity is easier to work on. If someone uses the company checkbook to write a check to themselves and embezzle money, we reduce the opportunity by requiring two signatures on checks going forward.

We’ve been working on opportunity (policies, rules, internal controls, audits) for a long time and yet employees still engage in wrongdoing.

Can someone please remind me of the definition of insanity?

I suggest it’s time to focus on pressure (both emotional and economic) and rationalization.

It’s time we re-think how we compensate our employees, how we weaponize data with scorecards that aim to shame our employees into performance, how we operationalize trust.

Addressing pressure and rationalization is a lot more difficult. But most compliance programs have reached the limit in terms of what additional controls can do. In fact, too many controls can add pressure and help rationalize bad behavior.

A good place to start on this new journey is outlined in a fantastic book titled Primed to Perform.

Look around. It’s clear that we need to start performing differently.

2 thoughts on “The forgotten sides of the fraud triangle”